Commercial banks and other financial institutions are an integral part of present economies. Individuals as well as public and private institutions can hardly operate without the institution of banking. Modern banking operations are primarily interest-centric. Banks receive money and lend it on interest. This is prohibited in Islam. Since interest permeates all the operations of the banking system, the whole banking system is repugnant to Muslims.

Islamic banking-as an alternative to the Western capitalist banking system-prohibits any kind of speculation, interest, and immoral investments (e.g. casinos). Islamic banks have to make a profit. They do this by buying assets on behalf of the customer, who has to repay the loan and a fee for using the asset. When the loan is paid off, the asset’s ownership is transferred to the borrower. The advantage of this arrangement is that the bank shares not only the profit but the risk as well. For this reason, it gets the opportunity

to have a close look at the potential borrowers.This book deals with conceptual, theoretical and empirical framework of Islamic banking system. It also provides a performance review of Islamic banks in global perspective. More importantly, it explains and examines the practices of Islamic banking in India, focusing on issues and constraints. Finally, it suggests the need for establishment of Islamic banks in India and areas of further research in the subject.

Author’s Profile

Dr. A. Abdul Raheem is presently Associate Professor, Department of Economics, The New College (Autonomous), Chennai. He did his M.Phil. and Ph.D. from Annamalai University, Tamil Nadu. He has contributed numerous research articles in reputed national and international journals and published 4 books. He successfully completed two research projects funded by University Grants Commission (UGC), New Delhi.

Dr. Raheem is recipient of distinguished scholar in economics award from Southern India Chamber of Commerce and Industry. His areas of research interest include micro finance, Islamic banking, rural development, and women empowerment.

Preface

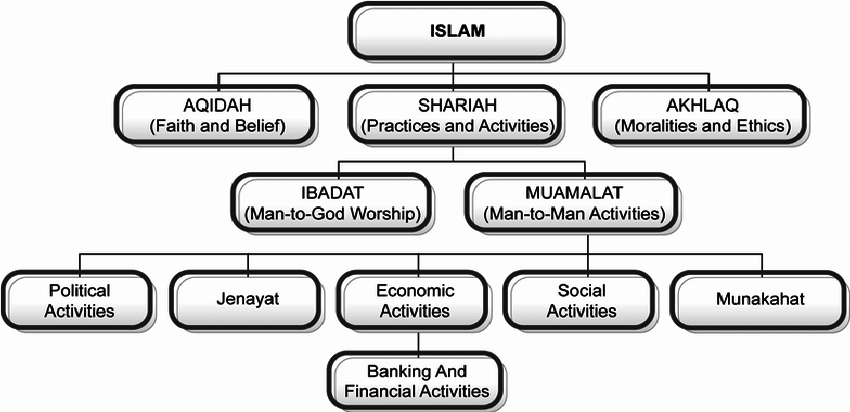

Islamic banks are banking institutions that provide the Islamic banks cannot offer a loan to earn interest or discount a banking services within the boundaries of Islamic principles. commercial bill or grant any drawing facilities. Further, Islamic banks are not allowed to deal in swaps of different currencies because of the involvement of the interest between the two currencies that are exchanged on forward basis. The Islamic banking system draws a clear distinction between services and financing activities.

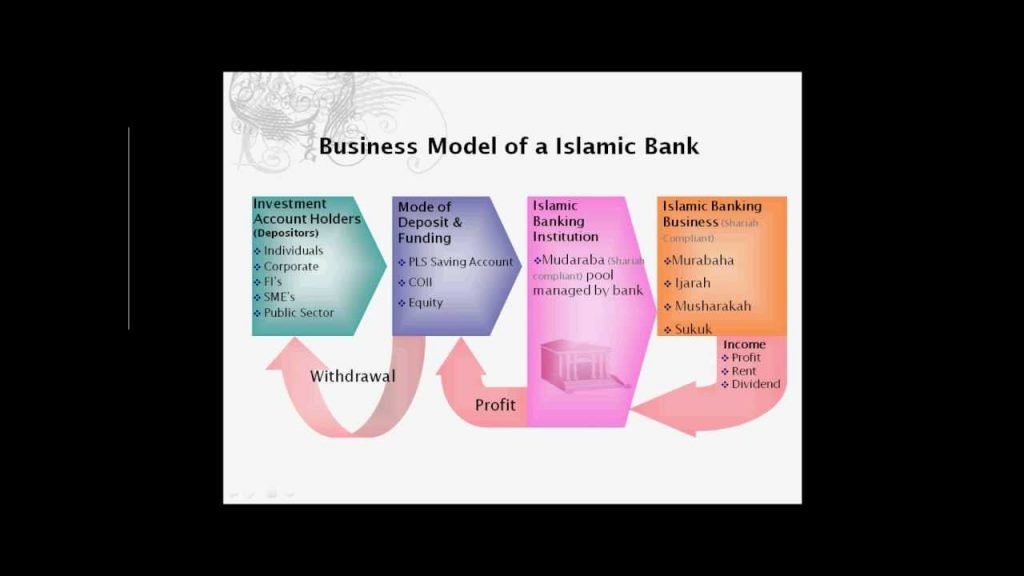

According to Islamic principles, usury is forbidden and the Mudharabah system is commonly used as a vehicle for investment especially for those people who cannot do the job themselves, like the soldiers, orphans or government officials. Scholars in different sectors and school of thought recognized Al-Mudharabah contract as an accepted deal. In later stage, development of Muslim society witnessed a third party who could work as a mediatory between the providers of the capital and the beneficiaries. The third party will be a trustworthy person who used to take the money from those who were looking for investment. The new thing is that the trusted person did not work by himself but he used to give such money to a qualified person who could do the job. The profit of the trusted person is derived from the difference between the percentage he agrees to take from the owner of the capital (say 50 percent of the realized profit) and the percentage that he can impose on the user of the borrowed money (say 60 percent). The trusted person in his role as a mediator will play the same role as it is played now by the modern banks, i.e. taking the deposit to use the same to others. Under this system of single and double Mudharabah contracts, a long lasting civilization did arise under the umbrella of Islam.

For millions of Muslims, banks are institutions to be avoided. Their Islamic beliefs prevent them from the dealings that involve usury or interest (riba). Yet, Muslims need banking services for many purposes as much as anyone else needs, and to

finance new business ventures, to buy a house, to buy a car, to facilitate capital investment, to undertake trading activities or to offer a safe place for savings. For Muslims who are not averse to legitimate profit as Islam encourages people to use money in Islamically legitimate ventures, not just to keep their funds idle. Islamic banking, based on the Qur’anic prohibition of charging interest, has moved from a theoretical concept to embracing more than 300 Islamic financial institutions, which operate worldwide in about 75 countries. Patrons of Islamic banking and finance are not confined to Muslim countries but are also spreading over Europe, the United States, the Far East, South Asia and the Middle East. Assets of Islamic banks worldwide are estimated to be more than US$ 265 billion and of financial investments above US$ 400 billion. Islamic bank deposits are estimated at over US$ 202 billion worldwide with a growth rate between 10 and 20 percent. The best known feature of Islamic banking is the prohibition of interest. The Qur’an forbids charging of riba (an Arabic term having a wider meaning than Interest) on money lent. It is important to understand certain principles of Islam that undermine Islamic finance.

Contents

Introduction

1. Islamic Banking System

1.2 Need for an Islamic Banking System

1.3 Concept of Islamic Banking

1.4 Major Channels of an Islamic Bank

1.4.1 Mudharabah (A Method of Trust Financing)

1.4.2 Musharakah (Which Covers Equity Participation and Decreased Participation)

1.4.3 Murabaha (Cost plus Profit Margin in Trade or Other Financing)

1.5. Functions and Dimensions of an Islamic Bank

1.6 Conventional Banks versus Islamic Banks

1.6.1 Similarities

1.6.2 Differences

1.7 Structure of Islamic Banks

1.7.1 Banking Operations

1.7.2 Investment and Financing

1.7.3 Legal and Fiqhi Jurisprudence

1.7.4 Financial Control Administration (including Training and O&M)

1.7.5 Planning, Research and Development

1.7.6 Control

1.7.7 Social Activities and Community Services Islamic Banking

1.8 Islamic Bank: Some Critical Issues

1.8.1 Marketing

1.8.2 Partnership Balances

1.8.3 Financial Standards and Reporting

1.8.4 Relaionship with Reguatory Authority

1.8.5 Aspects of Relationship

1.8.6 Interest-free Commercial Banking

1.8.7 Quality in Service

2. Islamic Banking: Theoretical Framework

2.1 Introduction

2.2 Models of Islamic Banking

2.3 Viability of Islamic Banking

2.4 Socio-economic Consequences of Islamic Banking

2.4.1 Effects on Saving and Investment

2.4.2 Impact on the Rate and Pattern of Growth

2.4.3 Impact on Allocative Efficiency

2.4.4 Consequences for the Stability of the Banking System

2.4.5 Effects on the Stability of the Economic System

2.5 The Practice of Islamic Banking

2.5.1 Practice of Islamic Banking: Individual Entities

2.6 Conclusion

3. Islamic Banking: Conceptual and Empirical Framework

3.1 Evolution of Islamic Banking

3.1.1 Shari’ah Principles

3.2 Essential Feature of Islamic Banking

3.3 Anatomy of Islamic Banking

3.4 Islamic Banking: Conceptual Framework

3.4.1 Islamic Banking

3.4.2 Riba

3.4.3 Mudarabah (Passive Partnership)

3.4.4 Musharakah (Active Partnership)

3.4.5 Diminishing Partnership

3.4.6 Murabahah (Sales Contract at a Profit Mark-up)

3.4.7 Ijara (Leasing)

4. Islamic Financial Institutions/Banks: A Global View

4.1 Introduction

4.2 Performance of Islamic Financial Institutions (IFIs)

4.2.1 Number of Islamic Financial Institutions

4.2.2 Geographical Spread of Islamic Financial Institutions

4.2.3 Progress in the Establishment of IFIs

4.3 Evaluation of Islamic Financial Institution

4.3.1 IFIS Total Assets

4.3.2 IFIs Assets: Country-wise

4.3.3 IFIs Assets: Institution-wise

4.3.4 Total Deposits in IFIs

4.3.5 Growth of Current Accounts

4.3.6 IFIs Shareholders’ Equity

4.3.7 IFIs Shareholders’ Equity: Country-wise

4.3.8 IFIs Shareholders’ Equity: Institution-wise

4.3.9 IFIs Net Profit and Reserves

4.9.10 IFIS Total Investments

4.9.11 IFIs Return on Equity ROE

4.9.12 ROE: Regional and Country-wise

4.4 Performance of Islamic Banks: The Case of Bank Islam Malaysia Berhad (BIMB)

4.4.1 Variations in Financial Performance Indicators of BIMB

4.4.2 Growth Trends in Financial Performance Indicators of BIMB

5. Islamic Banking in India: Issues and Constraints